UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| (Mark One) | |

| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2017. | |

| OR | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Date of event requiring this shell company report. . . . . . . . . . . . . . | |

Commission file number: 001-33768

FANHUA INC.

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

Cayman Islands

(Jurisdiction of incorporation or organization)

27/F, Pearl River Tower

No. 15 West Zhujiang Road

Guangzhou, Guangdong 510623

People’s Republic of China

(Address of principal executive offices)

Peng Ge, Chief Financial Officer

Tel: +86 20 83883033

E-mail: gepeng@fanhuaholdings.com

Fax: +86 20 83883181

27/F, Pearl River Tower

No. 15 West Zhujiang Road

Guangzhou, Guangdong 510623

People’s Republic of China

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

|

Ordinary shares, par value US$0.001 per share* American depositary shares, each representing 20 ordinary shares |

The NASDAQ Stock Market LLC (The NASDAQ Global Select Market) |

*Not for trading, but only in connection with the listing on The NASDAQ Global Select Market of American depositary shares, each representing 20 ordinary shares.

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the Issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

1,300,191,084 ordinary shares, par value US$0.001 per share as of December 31, 2017

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☒ No ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☐ | Accelerated filer ☒ |

| Non-accelerated filer ☐ | Emerging growth company ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards † provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☒ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ |

Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes ☐ No ☐

TABLE OF CONTENTS

In this annual report, unless the context otherwise requires:

| · | “we,” “us,” “our company,” “our” or “Fanhua” refer to Fanhua Inc., formerly known as CNinsure Inc., its subsidiaries and our consolidated affiliated entities, if applicable; |

| · | “China” or “PRC” refers to the People’s Republic of China, excluding, solely for the purpose of this annual report, Taiwan, Hong Kong and Macau; |

| · | “provinces” of China refers to the 22 provinces, the four municipalities directly administered by the central government (Beijing, Shanghai, Tianjin and Chongqing), the five autonomous regions (Xinjiang, Tibet, Inner Mongolia, Ningxia and Guangxi); |

| · | “shares” or “ordinary shares” refers to our ordinary shares, par value US$0.001 per share; |

| · | “ADSs” refers to our American depositary shares, each of which represents 20 ordinary shares; |

| · | all references to “RMB” or “Renminbi” are to the legal currency of China, all references to “US$” and “U.S. dollars” are to the legal currency of the United States and all references to “HK$” and “HK dollars” are to the legal currency of the Hong Kong Special Administrative Region; and |

| · | all discrepancies in any table between the amounts identified as total amounts and the sum of the amounts listed therein are due to rounding. |

| Item 1. | Identity of Directors, Senior Management and Advisers |

Not Applicable.

| Item 2. | Offer Statistics and Expected Timetable |

Not Applicable.

| Item 3. | Key Information |

| A. | Selected Financial Data |

In November 2017, we disposed of Fanhua Bocheng Insurance Brokerage Co., Ltd., or Bocheng, which is the primary operating entity of our insurance brokerage segment. Accordingly, the insurance brokerage segment was accounted as discontinued operations. Consolidated statements of operations for the years ended 2013, 2014, 2015 and 2016 have been restated to conform to the current presentation.

The following selected consolidated statements of income data for the years ended December 31, 2015, 2016 and 2017 and the consolidated balance sheets data as of December 31, 2016 and 2017 have been derived from our audited consolidated financial statements, which are included in this annual report beginning on page F-1. The selected consolidated statements of income data for the years ended December 31, 2013 and 2014 and the selected consolidated balance sheets data as of December 31, 2013, 2014 and 2015 have been derived from our consolidated financial statements, which are not included in this annual report.

Our historical results do not necessarily indicate results expected for any future periods. The selected consolidated financial data should be read in conjunction with, and are qualified in their entirety by reference to, our audited consolidated financial statements and related notes and “Item 5. Operating and Financial Review and Prospects” below. Our audited consolidated financial statements are prepared and presented in accordance with U.S. GAAP.

| -1- |

| For the Year Ended December 31, | ||||||||||||||||||||||||

| 2013 | 2014 | 2015 | 2016 | 2017 | ||||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | US$ | |||||||||||||||||||

| (in thousands, except shares, per share and per ADS data) | ||||||||||||||||||||||||

| Consolidated Statements of Income Data | ||||||||||||||||||||||||

| Net revenues: | ||||||||||||||||||||||||

| Agency | 1,418,512 | 1,624,410 | 2,155,264 | 3,746,471 | 3,780,217 | 581,008 | ||||||||||||||||||

| Life insurance business | 199,421 | 197,208 | 319,916 | 990,541 | 2,424,444 | 372,630 | ||||||||||||||||||

| P&C insurance business | 1,219,091 | 1,427,202 | 1,835,348 | 2,755,930 | 1,355,773 | 208,378 | ||||||||||||||||||

| Claims adjusting | 261,206 | 292,981 | 303,846 | 336,413 | 308,256 | 47,378 | ||||||||||||||||||

| Others | 13,888 | — | — | — | — | — | ||||||||||||||||||

| Total net revenues | 1,693,606 | 1,917,391 | 2,459,110 | 4,082,884 | 4,088,473 | 628,386 | ||||||||||||||||||

| Operating costs and expenses: | ||||||||||||||||||||||||

| Agency | (1,094,843 | ) | (1,261,887 | ) | (1,675,262 | ) | (2,906,791 | ) | (2,864,882 | ) | (440,324 | ) | ||||||||||||

| Life insurance business | (138,982 | ) | (129,357 | ) | (205,313 | ) | (673,230 | ) | (1,636,340 | ) | (251,501 | ) | ||||||||||||

| P&C insurance business | (955,861 | ) | (1,132,530 | ) | (1,469,949 | ) | (2,233,561 | ) | (1,228,542 | ) | (188,823 | ) | ||||||||||||

| Claims adjusting | (142,245 | ) | (167,676 | ) | (181,370 | ) | (199,810 | ) | (194,525 | ) | (29,898 | ) | ||||||||||||

| Others | (8,933 | ) | — | — | — | — | — | |||||||||||||||||

| Total operating costs | (1,246,021 | ) | (1,429,564 | ) | (1,856,632 | ) | (3,106,601 | ) | (3,059,407 | ) | (470,222 | ) | ||||||||||||

| Selling expenses | (95,990 | ) | (105,169 | ) | (125,041 | ) | (502,802 | ) | (221,785 | ) | (34,088 | ) | ||||||||||||

| General and administrative expenses(1) | (343,308 | ) | (387,362 | ) | (448,989 | ) | (481,947 | ) | (534,145 | ) | (82,096 | ) | ||||||||||||

| Total operating costs and expenses | (1,685,319 | ) | (1,922,095 | ) | (2,430,662 | ) | (4,091,350 | ) | (3,815,337 | ) | (586,406 | ) | ||||||||||||

| Income (loss) from continuing operations | 8,287 | (4,704 | ) | 28,448 | (8,466 | ) | 273,136 | 41,980 | ||||||||||||||||

| Other income, net: | ||||||||||||||||||||||||

| Investment income | 8,886 | 44,240 | 65,624 | 115,275 | 191,784 | 29,477 | ||||||||||||||||||

| Interest income | 84,214 | 82,216 | 57,206 | 6,901 | 25,891 | 3,980 | ||||||||||||||||||

| Others, net | (4,601 | ) | 2,030 | 20,964 | 10,341 | 14,284 | 2,195 | |||||||||||||||||

| Income from continuing operations before income taxes, share of income of affiliates and discontinued operations | 96,786 | 123,782 | 172,242 | 124,051 | 505,095 | 77,632 | ||||||||||||||||||

| Income tax expense | (26,924 | ) | (23,637 | ) | (25,553 | ) | (27,249 | ) | (167,803 | ) | (25,791 | ) | ||||||||||||

| Share of income of affiliates | 20,621 | 30,649 | 26,924 | 48,293 | 108,944 | 16,744 | ||||||||||||||||||

| Net income from continuing operations | 90,483 | 130,794 | 173,613 | 145,095 | 446,236 | 68,585 | ||||||||||||||||||

| Net income from discontinued operations, net of tax | 9,501 | 35,286 | 41,868 | 22,543 | 5,480 | 842 | ||||||||||||||||||

| Net income | 99,984 | 166,080 | 215,481 | 167,638 | 451,716 | 69,427 | ||||||||||||||||||

| Less: Net income attributable to the noncontrolling interests | 4,341 | 4,320 | 5,395 | 10,591 | 2,488 | 382 | ||||||||||||||||||

| Net income attributable to the Company’s shareholders | 95,643 | 161,760 | 210,086 | 157,047 | 449,228 | 69,045 | ||||||||||||||||||

| Net income per share: | ||||||||||||||||||||||||

| Basic: | ||||||||||||||||||||||||

| Net income from continuing operation | 0.09 | 0.13 | 0.14 | 0.12 | 0.36 | 0.06 | ||||||||||||||||||

| Net income from discontinued operation | 0.01 | 0.03 | 0.04 | 0.02 | 0.00 | 0.00 | ||||||||||||||||||

| Net income | 0.10 | 0.16 | 0.18 | 0.14 | 0.36 | 0.06 | ||||||||||||||||||

| Diluted: | ||||||||||||||||||||||||

| Net income from continuing operation | 0.09 | 0.13 | 0.14 | 0.11 | 0.36 | 0.06 | ||||||||||||||||||

| Net income from discontinued operation | 0.01 | 0.03 | 0.03 | 0.02 | 0.00 | 0.00 | ||||||||||||||||||

| Net income | 0.10 | 0.16 | 0.17 | 0.13 | 0.36 | 0.06 | ||||||||||||||||||

| Net income per ADS: | ||||||||||||||||||||||||

| Basic: | ||||||||||||||||||||||||

| Net income from continuing operation | 1.81 | 2.60 | 2.92 | 2.32 | 7.20 | 1.11 | ||||||||||||||||||

| Net income from discontinued operation | 0.11 | 0.62 | 0.73 | 0.39 | 0.09 | 0.02 | ||||||||||||||||||

| Net income | 1.92 | 3.22 | 3.65 | 2.71 | 7.29 | 1.13 | ||||||||||||||||||

| Diluted: | ||||||||||||||||||||||||

| Net income from continuing operation | 1.81 | 2.58 | 2.79 | 2.23 | 7.20 | 1.11 | ||||||||||||||||||

| Net income from discontinued operation | 0.10 | 0.61 | 0.70 | 0.37 | 0.09 | 0.02 | ||||||||||||||||||

| Net income | 1.91 | 3.19 | 3.49 | 2.60 | 7.29 | 1.13 | ||||||||||||||||||

| Shares used in calculating net income per share: | ||||||||||||||||||||||||

| Basic | 998,861,526 | 1,005,842,212 | 1,151,705,374 | 1,160,592,325 | 1,231,698,725 | 1,231,698,725 | ||||||||||||||||||

| Diluted | 1,000,570,018 | 1,012,591,387 | 1,203,323,521 | 1,208,821,796 | 1,261,223,049 | 1,261,223,049 | ||||||||||||||||||

_________________________

| (1) | Including share-based compensation expenses of RMB45.3 million, RMB23.6 million, RMB17.7 million, RMB4.9 million and nil for the years ended December 31, 2013, 2014, 2015, 2016 and 2017, respectively. |

| -2- |

| As of December 31, | ||||||||||||||||||||||||

| 2013 | 2014 | 2015 | 2016 | 2017 | ||||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | US$ | |||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||

| Consolidated Balance Sheet Data: | ||||||||||||||||||||||||

| Cash and cash equivalents | 2,284,847 | 2,099,468 | 1,115,172 | 236,952 | 363,746 | 55,907 | ||||||||||||||||||

| Total current assets | 3,177,801 | 3,301,726 | 3,513,061 | 3,694,564 | 4,132,527 | 635,158 | ||||||||||||||||||

| Total assets | 3,560,730 | 3,748,486 | 4,014,428 | 4,238,568 | 4,737,742 | 728,178 | ||||||||||||||||||

| Total current liabilities | 339,425 | 335,440 | 488,448 | 747,119 | 661,860 | 101,725 | ||||||||||||||||||

| Total liabilities | 413,968 | 414,226 | 580,859 | 834,474 | 749,349 | 115,172 | ||||||||||||||||||

| Noncontrolling interests | 118,665 | 123,508 | 116,139 | 117,242 | 111,342 | 17,113 | ||||||||||||||||||

| Total equity | 3,146,762 | 3,334,260 | 3,433,569 | 3,404,094 | 3,988,393 | 613,006 | ||||||||||||||||||

| Total liabilities and shareholders’ equity | 3,560,730 | 3,748,486 | 4,014,428 | 4,238,568 | 4,737,742 | 728,178 | ||||||||||||||||||

Exchange Rate Information

Our business is primarily conducted in China and all of our revenues are denominated in RMB. This annual report contains translations of RMB amounts into U.S. dollars at specific rates solely for the convenience of the readers. Unless otherwise noted, all translations from RMB to U.S. dollars in this annual report were made at a rate of RMB 6.5063 to US$1.00, the noon buying rate in effect as of December 29, 2017 in The City of New York for cable transfers of RMB, as set forth in H.10 weekly statistical release of the Federal Reserve Bank of New York. We make no representation that any RMB or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or RMB, as the case may be, at any particular rate, or at all. The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of RMB into foreign exchange and through restrictions on foreign trade. On April 13, 2018, the noon buying rate was RMB6.2725 to US$1.00.

The following table sets forth information concerning exchange rates between the RMB and the U.S. dollar for the periods indicated. These rates are provided solely for your convenience and are not necessarily the exchange rates that we used in this annual report or will use in the preparation of our future periodic reports or any other information to be provided to you.

| -3- |

| Noon Buying Rate | ||||||||||||||||

| (RMB per US$1.00) | ||||||||||||||||

| Period | Period End | Average(1) | Low | High | ||||||||||||

| 2013 | 6.0537 | 6.1412 | 6.2438 | 6.0537 | ||||||||||||

| 2014 | 6.2046 | 6.1704 | 6.2591 | 6.0402 | ||||||||||||

| 2015 | 6.4778 | 6.2869 | 6.4896 | 6.1870 | ||||||||||||

| 2016 | 6.9430 | 6.6549 | 6.9580 | 6.4480 | ||||||||||||

| 2017 | ||||||||||||||||

| October | 6.6328 | 6.6254 | 6.6533 | 6.5712 | ||||||||||||

| November | 6.6090 | 6.6200 | 6.6385 | 6.5967 | ||||||||||||

| December | 6.5063 | 6.5932 | 6.6210 | 6.5063 | ||||||||||||

| 2018 | ||||||||||||||||

| January | 6.2841 | 6.4233 | 6.5263 | 6.2841 | ||||||||||||

| February | 6.3280 | 6.3183 | 6.3471 | 6.2649 | ||||||||||||

| March | 6.2726 | 6.3174 | 6.3565 | 6.2685 | ||||||||||||

| April (through April 13) | 6.2725 | 6.2889 | 6.3045 | 6.2655 | ||||||||||||

_____________________________

Source: H.10 weekly statistical release of the Federal Reserve Bank of New York

| (1) | Annual averages are calculated from month-end rates. Monthly averages are calculated using the average of the daily rates during the relevant period. |

| B. | Capitalization and Indebtedness |

Not Applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not Applicable.

| D. | Risk Factors |

Risks Related to Our Business and Our Industry

If and when our contracts with insurance companies are suspended or changed, our business and operating results will be materially and adversely affected.

We primarily act as agents for insurance companies in distributing their products to retail customers. We also provide claims adjusting services principally to insurance companies. Our relationships with the insurance companies are governed by agreements between us and the insurance companies. We have entered into strategic partnership agreements with most of our major insurance company partners for the distribution of life, property and casualty insurance products and the provision of claims adjusting services at the corporate headquarters level. While this approach allows us to obtain more favorable terms from insurance companies by combining the sales volumes and service fees of our affiliated insurance agencies and claims adjusting firms, it also means that the termination of a major contract could have a material adverse effect on our business. Under the framework of the headquarter-to-headquarter agreements, our affiliated insurance agencies and claims adjusting firms generally also enter into contracts at a local level with the respective provincial, city and district branches of the insurance companies. Generally, each branch of these insurance companies has independent authority to enter into contracts with our affiliated insurance agencies and claims adjusting firms, and the termination of a contract with one branch has no significant effect on our contracts with the other branches. See “Item 4. Information on the Company — B. Business Overview — Insurance Company Partners.” These contracts establish, among other things, the scope of our authority, the pricing of the insurance products we distribute and our fee rates. These contracts typically have a term of one year and certain contracts can be terminated by the insurance companies with little advance notice. Moreover, before or upon expiration of a contract, the insurance company that is a party to that contract may agree to renew it only with changes in material terms, including the amount of commissions and fees we receive, which could reduce our revenues from that contract.

For the year ended December 31, 2017, our top five insurance company partners were Huaxia Life Insurance Co., Ltd., or Huaxia, Tian'an Life Insurance Co., Ltd., or Tian'an, China Pacific Property Insurance Co., Ltd., or CPIC, Ping An Property & Casualty Insurance Company of China, Ltd., or Ping An and PICC Property and Casualty Company Limited, or PICC P&C. Among these top five partners, each of Huaxia and Tian'an accounted for more than 10% of our total net revenues individually in 2017, with Huaxia accounting for 24.2% and Tian'an for 22.3%.

| -4- |

On March 1, 2017, our subsidiaries were notified verbally by PICC P&C's local branches that PICC P&C was temporary suspending its business cooperation with us on areas such as insurance agency, brokerage and claims adjustment because certain of PICC P&C’s senior management members were being investigated by the government. We have resumed our business cooperation with PICC P&C in certain regions during the fourth quarter of 2017 and have resumed the settlement of the account receivables from PICC P&C. Part of PICC P&C related receivables were transferred to the buyer at the time of the disposal of the P&C entities. For further information on this disposal, please see “Item 4. – Information on the Company – C. Organizational Structure – Recent Principal Changes in Corporate Structure ”.

If our investments in our mobile and online platforms are not successful, our business and results of operations may be materially and adversely affected.

We have devoted significant efforts to developing and managing our mobile and online platforms. On January 1, 2012, we launched Baowang (www.baoxian.com), an online insurance platform which allows customers to search for and purchase a wide range of insurance products, including travel insurance, accident insurance and homeowner insurance from various insurance carriers. In October 2012, we launched CNpad Auto, the mobile workstation of our proprietary sales support system, which enables sales agents to help their clients compare prices, policy benefits and services from different insurance carriers’ auto insurance policies, and to apply for and complete the purchase of the policy that best suits their clients’ needs anywhere and anytime. In August 2014, we unveiled eHuzhu (www.ehuzhu.com), an online non-profit mutual aid platform that provides low-cost risk-protection programs on a mutual aid basis among program members. In August 2014, we also rolled out Chetong.net (www.chetong.net), an online-to-offline public service platform for the insurance industry that integrates claims adjustment and auto service resources from around the country to provide claims services such as damage assessment and loss estimations. In 2015, we sold approximately 80% of the equity interests in the operating entity of Chetong.net to its management and employees. In September 2017, we launched Lan Zhanggui, an internet-based all-in-one platform which integrates several of our existing online platforms and allows our agents to access and purchase a wide variety of insurance products, including life insurance, auto insurance, accident insurance, travel insurance and standard health insurance products from multiple insurance companies on their mobile devices. In the next few years, we intend to continue to devote significant resources to improving the technology and content of our existing online and mobile initiatives. However, our efforts to develop our mobile and online platforms may not be successful or yield the benefits that we anticipate. In addition, our expansion may depend on a number of factors, many of which are beyond our control, including but not limited to:

| · | the effectiveness of our marketing campaigns to build brand recognition among consumers and our ability to attract and retain customers; |

| · | the acceptance of third-party e-commerce platforms as an effective channel for underwriters to distribute their insurance products; |

| · | the acceptance of CNpad Auto and Lan Zhanggui as effective tools for sales agents; |

| · | public concerns over security of e-commerce transactions and confidentiality of information; |

| · | increased competition from insurance companies which directly sell insurance products through their own websites, call centers, portal websites which provide insurance product information and links to insurance companies’ websites, and other professional insurance intermediary companies which may launch independent websites in the future; |

| · | further improvement in our information technology system designed to facilitate smoother online transactions; and |

| · | further development and changes in applicable rules and regulations which may increase our operating costs and expenses, impede the execution of our business plan or change the competitive landscape. |

| -5- |

On July 27, 2015, the China Insurance Regulatory Commission, or CIRC, promulgated the Interim Measures for the Supervision of Internet Insurance Business, or Interim Measures, which immediately became effective and sets forth the qualifications and procedures for insurance intermediaries to operate internet insurance businesses in China. As advised by our PRC counsel, we have obtained the necessary approvals and licenses and our operations meet the qualification requirements of the Interim Measures. Since online insurance distribution has emerged only recently in China and is evolving rapidly, the CIRC may promulgate and implement new laws and regulations to govern this sector from time to time. We cannot assure you that our operations will always be consistent with the changes and further development of regulations applicable to us or we will be able to obtain necessary approvals and licenses as required on a timely basis.

Any failure to successfully identify the risks as part of our expansion into the online and mobile insurance distribution business may have a material adverse impact on our growth, business prospects and results of operations, which could lead to a decline in the price of our ADSs.

In addition, our efforts to enhance our technological capabilities and establish a leading position in the online and mobile insurance distribution and online claims settlement markets require us to incur significant research and development and marketing expenses which may adversely impact our profitability in the near term.

If we fail to attract and retain productive agents, especially entrepreneurial agents, and qualified claims adjustors, our business and operating results could be materially and adversely affected.

A substantial portion of our sales of property and casualty insurance products and all of our sales of life insurance products are conducted through our individual sales agents, who are not our employees. Some of these sales agents are significantly more productive than others in generating sales. In recent years, some entrepreneurial management staff or senior sales agents of major insurance companies in China have chosen to leave their employers or principals and become independent agents. We refer to these individuals as entrepreneurial agents. An entrepreneurial agent is usually able to assemble and lead a team of sales agents. We have been actively recruiting and will continue to recruit entrepreneurial agents to join our distribution and service network as our sales agents. Entrepreneurial agents have been instrumental to the development of our life insurance business. In addition, we rely entirely on our in-house claims adjustors to provide claims adjusting services. Because claims adjustment requires technical skills, the technical competence of claims adjustors is essential to establishing and maintaining our brand image and relationships with our customers. If we are unable to attract and retain the core group of highly productive sales agents, particularly entrepreneurial agents, and qualified claims adjustors, our business could be materially and adversely affected. Competition for sales personnel and claims adjustors from insurance companies and other insurance intermediaries may also force us to increase the compensation of our sales agents, in-house sales representatives and claims adjustors, which would increase operating costs and reduce our profitability.

Because our industry is highly regulated, any material changes in the regulatory environment could change the competitive landscape of our industry or require us to change the way we do business. The administration, interpretation and enforcement of the laws and regulations currently applicable to us could change rapidly. If we fail to comply with applicable laws and regulations, we may be subject to civil and criminal penalties or lose the ability to conduct business with our clients, which could materially and adversely affect our business and results of operations.

We operate in a highly regulated industry. The laws and regulations applicable to us are evolving and may change rapidly. We could be required to spend significant time and resources in complying with any material changes in the regulatory environment, which could change the competitive environment of our industry significantly and cause us to lose some or all of our competitive advantages. The attention of our management team could be diverted to these efforts to comply or cope with an evolving regulatory or competitive environment. For example, the PRC Insurance Law and related regulations were amended in 2002, 2009, 2014 and 2015. The 2015 amendments involved a number of significant changes to the regulatory regime, including eliminating the requirement for any insurance agent, broker or claims adjusting practitioners to obtain a qualification certificate issued by the CIRC. The elimination of the certificate requirement may result in an increase in competition for our business and in misconduct by sales or service persons, in particularly sales misrepresentation. In addition, the general increase misconduct in the industry could potentially harm the reputation of the industry and have an adverse impact on our business.

On March 13, 2018, CIRC and CBRC were merged to form the Chinese Banking and Insurance Regulatory Committee (“CBIRC”). This new organization replaced the CIRC as the regulatory authority for the supervision of the Chinese insurance industry. There is uncertainty as to how the regulatory environment might change as a result of the merger. If we fail to adapt to new rules and regulations promulgated by the CBIRC, it could adversely affect our business and results of operations.

| -6- |

The CBIRC and its predecessor have extensive authority to supervise and regulate the insurance industry in China. In exercising its authority, the CIRC and CBIRC are given wide discretion, and the administration, interpretation and enforcement of the laws and regulations applicable to us involve uncertainties that could materially and adversely affect our business and results of operations. The People’s Bank of China and other government agencies may promulgate new rules governing online financial services. In July 2015, ten government agencies including the People’s Bank of China, the Ministry of Finance and CIRC promulgated a guidance letter on how to promote the healthy growth of internet financial services, which set forth the principles of supervising based on the rule of law, appropriate level of regulation, proper categorization, cooperation among different government agencies and promoting innovation. Not only may the laws and regulations applicable to us change rapidly, but it is sometimes unclear how they apply to our business. For example, the laws and regulations applicable to our online and mobile platforms may be unclear. Errors created by our products or services may be determined or alleged to be in violation of the applicable laws and regulations. Any failure of our products or services to comply with these laws and regulations could result in substantial civil or criminal liability; could adversely affect demand for our services; could invalidate all or portions of some of our customer contracts; could require us to change or terminate some portions of our business; could require us to refund portions of our services fees; could cause us to be disqualified from serving customers; and could have a material and adverse effect on our business.

Although we have not had any material violations to date, we cannot assure you that our operations will always comply with the interpretation and enforcement of the laws and regulations implemented by the CBIRC. Any determination by a provincial or national government agency that our activities or those of our vendors or customers violate any of these laws could subject us to civil or criminal penalties, could require us to change or terminate some portions of our operations or business, or could disqualify us from providing services to insurance companies or other customers; and, thus could have an adverse effect on our business.

Our business could be negatively impacted if we are unable to adapt our services to regulatory changes in China.

China’s insurance regulatory regime is undergoing significant changes. Some of these changes and the further development of regulations applicable to us may result in additional restrictions on our activities or more intensive competition in this industry. For example, both the Provisions on the Supervision of Professional Insurance Agencies and the Provisions on the Supervision of Insurance Brokerages were amended in December 2015. Pursuant to these amendments, an insurance agency or brokerage firm is allowed to apply for a business permit from the CIRC and a business license from the local administration of industry and commerce, or AIC, simultaneously while previously an insurance agency or brokerage firm had to obtain a business permit issued by the CIRC before it could apply for a business license from and register with the relevant local AIC. Prior approval by the CIRC is no longer required for an insurance agency or brokerage firm to establish or divest a branch office or subsidiary. In addition, pursuant to the amendment to the Provisions on the Supervision of Insurance Claims Adjusting Firms, insurance claim adjusting firms are no longer required to have a minimum registered capital of RMB2 million. See “Item 4. Information on the Company — B. Business Overview — Regulation.” While these changes may enable us to expand our branches more rapidly, it may also accelerate the growth of professional insurance intermediaries in China and intensify competition among insurance agencies, insurance brokerage firms and claims adjusting firms. Our business operations and growth outlook could be materially and adversely affected if we cannot adapt our business to the regulatory and industry changes.

We may be unsuccessful in identifying and acquiring suitable acquisition candidates, which could adversely affect our growth.

We may pursue acquisition of companies that can complement our existing business, diversify our product offerings and improve our customers’ experience in the future. However, there is no assurance that we can successfully identify suitable acquisition candidates. Even if we identify suitable candidates, we may not be able to complete an acquisition on terms that are commercially acceptable to us. Our competitors may be able to outbid us for these acquisition targets. If we are unable to complete acquisitions, our growth strategy may be impeded and our earnings or revenue growth may be negatively affected.

| -7- |

If we fail to integrate acquired companies efficiently, or if the acquired companies do not perform to our expectations, our business and results of operations may be adversely affected.

Even if we succeed in acquiring suitable target companies, our ability to integrate an acquired entity and its operations is subject to a number of factors. These factors include difficulties in the integration of acquired operations and retention of personnel, entry into unfamiliar markets, unanticipated problems or legal liabilities, tax and accounting issues. The need to address these factors may divert management’s attention from other aspects of our business and materially and adversely affect our business prospects. In addition, costs associated with integrating newly acquired companies could negatively affect our operating margins.

Furthermore, the acquired companies may not perform to our expectations for various reasons, including legislative or regulatory changes that affect the insurance products in which a company specializes, the loss of key clients after the acquisition closes, general economic factors that impact a company in a direct way and the cultural incompatibility of an acquired company’s management team with us. If an acquired company cannot be operated at the same profitability level as our existing operations, the acquisition would have a negative impact on our operating margin. Our inability to successfully integrate an acquired entity or its failure to perform to our expectations may materially and adversely affect our business, prospects, results of operations and financial condition.

Competition in our industry is intense and, if we are unable to compete effectively, we may lose customers and our financial results may be negatively affected.

The insurance intermediary industry in China is highly competitive, and we expect competition to persist and intensify. In insurance product distribution, we face competition from insurance companies that use their in-house sales force, exclusive sales agents, telemarketing and internet channels to distribute their products, and from business entities that distribute insurance products on an ancillary basis, such as commercial banks, postal offices and automobile dealerships, as well as from other professional insurance intermediaries. In our claims adjusting business, we primarily compete with other independent claims adjusting firms. We compete for customers on the basis of product offerings, customer services and reputation. Many of our competitors have greater financial and marketing resources than we do and may be able to offer products and services that we do not currently offer and may not offer in the future. The disruption of business cooperation with PICC P&C may cause us to lose our competitive advantages in certain areas. If we are unable to compete effectively against those competitors, we may lose customers and our financial results may be negatively affected.

Because the commission and fee revenue we earn on the sale of insurance products is based on premiums, commission and fee rates set by insurance companies, any decrease in these premiums, commission or fee rates may have an adverse effect on our results of operations.

We are engaged in the life insurance, property and casualty insurance and claims adjusting businesses and derive revenues primarily from commissions and fees paid by the insurance companies whose policies our customers purchase and to whom we provide claims adjusting services. The commission and fee rates are set by insurance companies and are based on the premiums that the insurance companies charge or the amount recovered from insurance companies. Commission and fee rates and premiums can change based on the prevailing economic, regulatory, taxation-related and competitive factors that affect insurance companies. These factors, which are not within our control, include the ability of insurance companies to place new business, underwriting and non-underwriting profits of insurance companies, consumer demand for insurance products, the availability of comparable products from other insurance companies at a lower cost, the availability of alternative insurance products such as government benefits and self-insurance plans, as well as the tax deductibility of commissions and fees and the consumers themselves. In addition, premium rates for certain insurance products, such as the mandatory automobile liability insurance that each automobile owner in the PRC is legally required to purchase, are tightly regulated by CIRC.

In October 2017 we started to implement a platform business model for auto insurance business. See “Item 4. Business Overview — Insurance Aggregator Site Partners” for a more detailed description of the platform business model. We derived a portion of the revenues from platform fees paid by businesses which distribute auto insurance products through our CNpad-based insurance aggregating platform. The platform fee rates are set at a certain percentage based on the insurance premiums transacted over CNpad. The fee rates can change based on the prevailing economic, regulatory, taxation-related and competitive factors that affect the third party aggregator sites which are not within our control.

| -8- |

Because we do not determine, and cannot predict, the timing or extent of premium or commission and fee rate changes, we cannot predict the effect any of these changes may have on our operations. Any decrease in premiums or commission and fee rates may significantly affect our profitability. In addition, our budget for future acquisitions, capital expenditures and other expenditures may be disrupted by unexpected decreases in revenues caused by decreases in premiums or commission and fee rates, thereby adversely affecting our operations.

Quarterly and annual variations in our commission and fee revenue may unexpectedly impact our results of operations.

Our commission and fee revenue is subject to both quarterly and annual fluctuations as a result of the seasonality of our business, the timing of policy renewals and the net effect of new and lost business. During any given year, our commission and fee revenue derived from distribution of property and casualty insurance products is highest during the fourth quarter and is lowest during the first quarter. Life insurance commission revenue is the highest in the first quarter and lowest in the fourth quarter of any given year as much of the Jumpstart Sales activities of life insurance companies occurs in January and February during which life insurance companies would increase their sales efforts by offering more incentives for insurance agents and insurance intermediaries to increase sales, while the preparation for the Jumpstart Sales starts in the fourth quarter of each year. The factors that cause the quarterly and annual variations are not within our control. Specifically, consumer demand for insurance products can influence the timing of renewals, new business and lost business, which generally includes policies that are not renewed, and cancellations. As a result, you may not be able to rely on quarterly or annual comparisons of our operating results as an indication of our future performance.

Our operating structure may make it difficult to respond quickly to operational or financial problems, which could negatively affect our financial results.

We currently operate through our wholly-owned or majority-owned insurance agencies and claims adjusting firms located in 30 provinces in China. These companies report their results to our corporate headquarters monthly. If these companies delay either reporting results or informing corporate headquarters of negative business developments such as losses of relationships with insurance companies, regulatory inquiries or any other negative events, we may not be able to take action to remedy the situation in a timely fashion. This in turn could have a negative effect on our financial results. In addition, if one of these companies were to report inaccurate financial information, we might not learn of the inaccuracies on a timely basis and be able to take corrective measures promptly, which could negatively affect our ability to report our financial results.

Our future success depends on the continuing efforts of our senior management team and other key personnel, and our business may be harmed if we lose their services.

Our future success depends heavily upon the continuing services of the members of our senior management team and other key personnel, in particular, Mr. Chunlin Wang, or Mr. Wang, our chairman of the board of directors and chief executive officer, and Mr. Peng Ge, or, Mr. Ge, our chief financial officer. If one or more of our senior executives or other key personnel, are unable or unwilling to continue in their present positions, we may not be able to replace them easily, or at all. As such, our business may be disrupted and our financial condition and results of operations may be materially and adversely affected. Competition for senior management and key personnel in our industry is intense because of a number of factors including the limited pool of qualified candidates. We may not be able to retain the services of our senior executives or key personnel, or attract and retain high-quality senior executives or key personnel in the future. As is customary in the PRC, we do not have insurance coverage for the loss of our senior management team or other key personnel.

In addition, if any member of our senior management team or any of our other key personnel joins a competitor or forms a competing company, we may lose customers, sensitive trade information, key professionals and staff members. Each of our executive officers and key employees has entered into an employment agreement with us which contains confidentiality and non-competition provisions. These agreements generally have an initial term of three years, and are automatically extended for successive one-year terms unless terminated earlier pursuant to the terms of the agreement. See “Item 6. Directors, Senior Management and Employees — A. Directors and Senior Management — Employment Agreements” for a more detailed description of the key terms of these employment agreements. If any disputes arise between any of our senior executives or key personnel and us, we cannot assure you of the extent to which any of these agreements may be enforced.

| -9- |

Salesperson and employee misconduct is difficult to detect and deter and could harm our reputation or lead to regulatory sanctions or litigation costs.

Salesperson and employee misconduct could result in violations of law by us, regulatory sanctions, litigation or serious reputational or financial harm. Misconduct could include:

| · | making misrepresentations when marketing or selling insurance to customers; |

| · | hindering insurance applicants from making full and accurate mandatory disclosures or inducing applicants to make misrepresentations; |

| · | hiding or falsifying material information in relation to insurance contracts; |

| · | fabricating or altering insurance contracts without authorization from relevant parties, selling false policies, or providing false documents on behalf of the applicants; |

| · | falsifying insurance agency business or fraudulently returning insurance policies to obtain commissions; |

| · | colluding with applicants, insureds, or beneficiaries to obtain insurance benefits; |

| · | engaging in false claims; or |

| · | otherwise not complying with laws and regulations or our control policies or procedures. |

On April 24, 2015, the PRC Insurance Law was amended and consequently on December 3, 2015, the CIRC amended the Provisions on the Supervision of Professional Insurance Agencies, the Provisions on the Supervision of Insurance Brokerages and the Provisions on the Supervision of Insurance Claims Adjusting Firms. These amendments have made a number of significant changes to the regulatory regime, including eliminating the requirement for an insurance agent, broker or claims adjusting practitioner to obtain a qualification certificate issued by the CIRC. The elimination of the certificate requirement may result in an increase in misconduct by sales or service persons, in particularly sales misrepresentation. We have internal policies and procedures to deter salesperson or employee misconduct. However, the measures and precautions we take to prevent and detect these activities may not be effective in all cases. We cannot assure you, therefore, that salesperson or employee misconduct will not lead to a material adverse effect on our business, results of operations or financial condition. In addition, the general increase in misconduct in the industry could potentially harm the reputation of the industry and have an adverse impact on our business.

Our investments in certain financial products may not yield the benefits we anticipate or incur financial loss, which could adversely affect our cash position.

In order to improve our return on capital, we may from time to time, upon board approval, invest certain portion of our cash in financial products, such as trust products, with terms of one to two years. These products may involve various risks, including default risks, interest risks, and other risks. We cannot guarantee these investments will yield the returns we anticipate and we could suffer financial loss resulting from the purchase of these financial products.

If we fail to maintain an effective system of internal controls over financial reporting, we may not be able to accurately report our financial results or prevent fraud.

We are subject to reporting obligations under U.S. securities laws. Pursuant to Section 404 of the Sarbanes-Oxley Act of 2002 and the related rules adopted by the Securities and Exchange Commission, or the SEC, every public company is required to include a management report on the company’s internal controls over financial reporting in its annual report, which contains management’s assessment of the effectiveness of the company’s internal controls over financial reporting. In addition, an independent registered public accounting firm must attest to and report on the effectiveness of the company’s internal controls over financial reporting.

Our management has concluded that our internal control over financial reporting was effective as of December 31, 2017. See “Item 15. Controls and Procedures.” However, there is no assurance that we will be able to maintain effective internal controls over financial reporting in the future. If we fail to do so, we may not be able to produce reliable financial reports and prevent fraud. Moreover, if we are not able to conclude that we have effective internal controls over financial reporting, investors may lose confidence in the reliability of our financial statements, which would negatively impact the trading price of our ADSs. Our reporting obligations as a public company, including our efforts to comply with Section 404 of the Sarbanes-Oxley Act, will continue to place a significant strain on our management, operational and financial resources and systems for the foreseeable future.

| -10- |

We may face legal action by former employers or principals of entrepreneurial agents who join our distribution and service network.

Competition for productive sales agents is intense within the Chinese insurance industry. When an entrepreneurial agent leaves his or her employer or principal to join our distribution and service network as our sales agent, we may face legal action by his or her former employer or principal of the entrepreneurial agent on the ground of unfair competition or breach of contract. As of the date of this annual report, there has been no such action filed or threatened against us. We cannot assure you that this will not happen in the future. Any such legal actions, regardless of merit, could be expensive and time-consuming and could divert resources and management’s attention from the operation of our business. If we were found liable in such a legal action, we might be required to pay substantial damages to the former employer or principal of the entrepreneurial agent, and our business reputation might be harmed. Moreover, the filing of such a legal action may discourage potential entrepreneurial agents from leaving their employers or principals, thus reducing the number of entrepreneurial agents we can recruit and potentially harming our growth prospects.

If we are unable to successfully expand into the consumer financial services and wealth management sectors, our business and results of operations may be adversely affected.

In order to better serve our customers’ needs for diversified and comprehensive financial services, we have expanded into complementary business areas, such as consumer finance and wealth management, to leverage our existing sales network, customer resources and operating platform. For example, in October 2009, we acquired 20.6% equity interest in Sincere Fame International Limited, or Sincere Fame, which owns 100% of the equity interests in China Financial Services Group Limited, or CFSG, a consumer financial services provider. In November 2010, we formed a joint venture, named Fanhua Puyi Investment Management Co., Ltd., or Puyi Investment, (which we later renamed as Fanhua Puyi Fund Sales Co. Ltd., or Puyi Fund Sales, after obtaining the license to distribute mutual funds in March 2013) in which we beneficially own 15.4% of the equity interests. Puyi Fund Sales is a financing platform for mutual funds and trust companies. If we decide to offer wealth management products in the future, our efforts to do so may not be successful and may subject us to risks associated with operating in the consumer financial services sectors in China, including but not limited to, changes in monetary or industry policies and other economic measures that may affect our cooperation with financial institutions and their product supply, as well as competition from other consumer credit brokerage companies and other financial services companies that offer wealth management products. Any failure to successfully identify, execute and integrate acquisitions, investments, joint ventures and alliances as part of any attempted expansion into the consumer financial services sector may have a material adverse impact on our growth, business prospects and results of operations, which could lead to a decline in the price of our ADSs.

If we are required to write down goodwill and other intangible assets, our financial condition and results may be materially and adversely affected.

When we acquire a business, the amount of the purchase price that is allocated to goodwill and other intangible assets is determined by the excess of the fair value of purchase price and any controlling interest over the net identifiable tangible assets acquired. As of December 31, 2017, goodwill represented RMB109.9 million (US$16.9 million), or 2.8% of our total shareholders’ equity, and other net intangible assets represented RMB17.2 million (US$2.6 million), or 0.4% of our total shareholders’ equity. Our management performs impairment assessment annually and we did not recognize any impairment loss between 2013 and 2017. Under current accounting standards, if we determine that goodwill or intangible assets are impaired, we will be required to write down the value of such assets and recognize corresponding impairment charges. As we implement our growth strategy through acquisitions, goodwill and intangible assets may comprise an increasingly larger percentage of our shareholders’ equity. As such, any write-down related to such goodwill and intangible assets may adversely and materially affect our shareholders’ equity and financial results.

| -11- |

Any significant failure in our information technology systems could have a material adverse effect on our business and profitability.

Our business is highly dependent on the ability of our information technology systems to timely process a large number of transactions across different markets and products at a time when transaction processes have become increasingly complex and the volume of such transactions is growing rapidly. The proper functioning of our financial control, accounting, customer database, customer service and other data processing systems, together with the communication systems of our various subsidiaries and our main offices in Guangzhou, is critical to our business and our ability to compete effectively. We cannot assure you that our business activities would not be materially disrupted in the event of a partial or complete failure of any of these primary information technology or communication systems, which could be caused by, among other things, software malfunction, computer virus attacks or conversion errors due to system upgrading. In addition, a prolonged failure of our information technology system could damage our reputation and materially and adversely affect our future prospects and profitability.

We may face potential liability, loss of customers and damage to our reputation for any failure to protect the confidential information of our customers.

Our customer database holds confidential information concerning our customers. We may be unable to prevent third parties, such as hackers or criminal organizations, from stealing information provided by our customers to us. Confidential information of our customers may also be misappropriated or inadvertently disclosed through employee misconduct or mistake. We may also in the future be required to disclose to government authorities certain confidential information concerning our customers.

In addition, many of our customers pay for our insurance services through third-party online payment services. In such transactions, maintaining complete security during the transmission of confidential information, such as personal information, is essential to maintaining consumer confidence. We have limited influence over the security measures of third-party online payment service providers. In addition, our third-party merchants may violate their confidentiality obligations and disclose information about our customers. Any compromise of our security or third-party service providers' security could have a material adverse effect on our reputation, business, prospects, financial condition and results of operations.

If we are accused of failing to protect the confidential information of our customers, we may be forced to expend significant financial and managerial resources in defending against these accusations and we may face potential liability. Any negative publicity may adversely affect our public image and reputation. In addition, any perception by the public that online commerce is becoming increasingly unsafe or that the privacy of customer information is vulnerable to attack could inhibit the growth of online services generally, which in turn may reduce the number of our customers.

If we are unable to respond in a timely and cost-effective manner to rapid technological change in the insurance intermediary industry, it may result in an adverse effect.

The insurance industry is increasingly influenced by rapid technological change, frequent new product and service introductions and evolving industry standards. For example, the insurance intermediary industry has increased use of the internet to communicate benefits and related information to consumers and to facilitate information exchange and transactions. We believe that our future success will depend on our ability to continue to anticipate technological changes and to offer additional product and service opportunities that meet evolving standards on a timely and cost-effective basis. There is a risk that we may not successfully identify new product and service opportunities or develop and introduce these opportunities in a timely and cost-effective manner. In addition, product and service opportunities that our competitors develop or introduce may render our products and services uncompetitive. As a result, we can give no assurances that technological changes that may affect our industry in the future will not have a material adverse effect on our business and results of operations.

We face risks related to health epidemics, severe weather conditions and other catastrophes, which could materially and adversely affect our business.

Our business could be materially and adversely affected by the outbreak of avian flu, severe acute respiratory syndrome, or SARS, another health epidemic, severe weather conditions or other catastrophes. In April 2009, influenza A (H1N1), a new strain of flu virus commonly referred to as “swine flu,” was first discovered in North America and quickly spread to other parts of the world, including China. In January and February 2008, a series of severe winter storms afflicted extensive damages and significantly disrupted people’s lives in large portions of southern and central China. In May 2008, an earthquake measuring 8.0 on the Richter scale hit Sichuan Province in southwestern China, causing huge casualties and property damages. In February 2013, H7N9 Avian influenza was first discovered in Shanghai, China and quickly widened its geographical spread in China. Because our business operations rely heavily on the efforts of individual sales agents, in-house sales representatives and claims adjustors, any prolonged recurrence of avian flu or SARS, or the occurrence of other adverse public health developments such as influenza A (H1N1) and Zika Virus, severe weather conditions such as the massive snow storms in January and February 2008 and other catastrophes such as the Sichuan earthquake may significantly disrupt our staffing and otherwise reduce the activity level of our work force, thus causing a material and adverse effect on our business operations.

| -12- |

Risks Related to Our Corporate Structure

If the PRC government finds that the structure for operating part of our China business does not comply with applicable PRC laws and regulations, we could be subject to severe penalties.

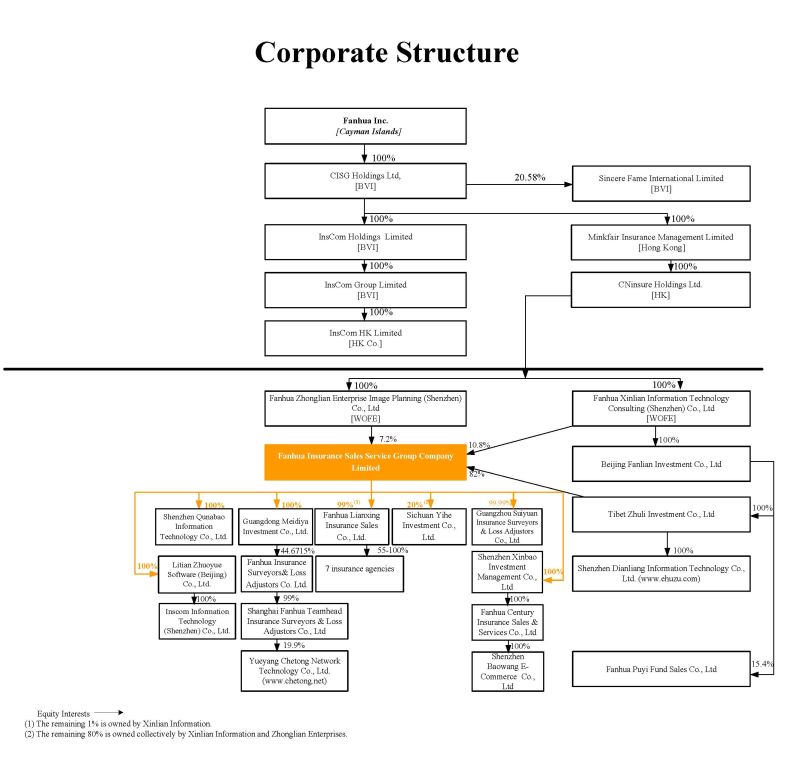

Historically, PRC laws and regulations have restricted foreign investment in and ownership of insurance intermediary companies. As a result, we conducted our insurance intermediary business through contractual arrangements among our PRC subsidiaries, consolidated affiliated entities including Xinbao Investment and Dianliang Information and their individual shareholders between December 2005 and May 2016.

In recent years, some rules and regulations governing the insurance intermediary sector in China have begun to encourage foreign investment. For instance, under the Closer Economic Partnership Arrangement, or CEPA, Supplement IV signed in July 2007 and CEPA Supplement VIII signed on December 13, 2011, between the PRC Ministry of Commerce and the governments of Hong Kong and Macao Special Administrative Region, local insurance agencies in Hong Kong and Macao are allowed to set up wholly-owned insurance agency companies in Guangdong Province if they meet certain threshold requirements. On December 26, 2007, the CIRC issued an Announcement on the Establishment of Wholly-owned Insurance Agencies in Mainland China by Hong Kong and Macao Insurance Agencies, which sets forth specific qualification criteria for implementation purposes. On August 26, 2010, the CIRC released a Circular on the Cancellation of the Fifth Batch of Administrative Approval Items, pursuant to which foreign ownership in a professional insurance intermediary in excess of 25% only requires a filing to be made with the relevant authorities and no longer requires prior approval. On March 13, 2015, the National Development and Reform Commission and Ministry of Commerce jointly issued the Catalogue for the Guidance of Foreign Investment Industries (Revision 2015), or the CGFII 2015 Revision, pursuant to which insurance brokerage firms are removed from the list of industries subject to foreign investment restriction.

We operated online insurance distribution business through Baoxian.com which was subject to foreign investment restriction. On June 19, 2015, the Ministry of Industry and Information Technology published a Notice on Removing the Foreign Ownership Restriction in Online Data Processing and Transaction Processing Business (Operating E-commerce), or the No. 196 Notice. Foreign ownership in online data processing and transaction process business is allowed to increase to 100% as long as the foreign-invested entities obtain necessary licenses to conduct the business. However, there remains uncertainty with regards to the implementation of the No. 196 Notice and the administrative procedures with regards to the application of the data processing and transaction process business licenses.

Following the changes in applicable foreign investment regulations, we commenced a restructuring of our company in October 2011 and subsequently terminated all the contractual arrangements among our PRC subsidiaries and consolidated entities such as Xinbao Investment and Dianliang Information, which became our wholly-owned subsidiaries in 2016. As a result, we obtained direct controlling equity ownership in all of our insurance intermediary companies and our online platforms in 2016. See “Item 4. Information on the Company — C. Organizational Structure.”

If our direct ownership of our online platforms is found to be in violation of any existing or future PRC laws or regulations, or fail to obtain or maintain any of the required permits or approvals, the relevant PRC regulatory authorities, including the CIRC, will have broad discretion in dealing with such violations, including:

| · | revoking the business and operating licenses of our PRC subsidiaries; |

| · | restricting or prohibiting any related-party transactions among our PRC subsidiaries; |

| -13- |

| · | imposing fines or other requirements with which we, our PRC subsidiaries may not be able to comply; |

| · | requiring us, our PRC subsidiaries to restructure the relevant ownership structure or operations; or |

| · | restricting or prohibiting us from providing additional funding for our business and operations in China. |

Any of these or similar actions could cause disruptions to our business, as well as reduce our revenues, profitability and cash flows.

In January 2015, the Ministry of Commerce, or the MOC, published a draft of the proposed Foreign Investment Law, which expands the definition of foreign investment and introduces the principle of “actual control” in determining whether a company is considered a foreign-invested enterprise, or an FIE. The draft Foreign Investment Law specifically provides that entities established in China but “controlled” by foreign investors will be treated as FIEs, whereas an entity set up in a foreign jurisdiction would nonetheless be, upon market entry clearance by the MOC, treated as a PRC domestic investor provided that the entity is “controlled” by PRC entities and/or citizens. In this connection, “control” is broadly defined in the draft law to cover the following summarized categories: (i) holding 50% of more of the voting rights of the subject entity; (ii) holding less than 50% of the voting rights of the subject entity but having the power to secure at least 50% of the seats on the board or other equivalent decision making bodies, or having the voting power to exert material influence on the board, the shareholders’ meeting or other equivalent decision making bodies; or (iii) having the power to exert decisive influence, via contractual or trust arrangements, over the subject entity’s operations, financial matters or other key aspects of business operations. Once an entity is determined to be an FIE, it will be subject to the foreign investment restrictions or prohibitions set forth in a “negative list,” to be separately issued by the State Council later, if the FIE is engaged in the industry listed in the negative list. Unless the underlying business of the FIE falls within the negative list, which calls for market entry clearance by the MOC, prior approval from the government authorities as mandated by the existing foreign investment legal regime would no longer be required for establishment of the FIE.

There is uncertainty regarding the draft Foreign Investment Law, including, the content of its final form and the timing of its adoption and implementation. It is uncertain whether the internet industry or online operation will be subject to the foreign investment restrictions or prohibitions set forth in the “negative list” to be issued. If the enacted version of the Foreign Investment Law and the final “negative list” mandate further actions, such as MOC market entry clearance, to be completed by companies, we face uncertainties as to whether such clearance can be timely obtained, or at all.

PRC regulation of loans and direct investment by offshore holding companies to PRC entities may delay or prevent us from making loans to our PRC subsidiaries or making additional capital contributions to our PRC subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business.

We are an offshore holding company conducting our operations in China through PRC subsidiaries in order to provide additional funding to our PRC subsidiaries, we may make loans to our PRC subsidiaries, or we may make additional capital contributions to our PRC subsidiaries.

Any loans we make to any of our directly-held PRC subsidiaries (which are treated as foreign-invested enterprises under PRC law), namely, Fanhua Zhonglian Enterprise Image Planning (Shenzhen) Co., Ltd., or Zhonglian Enterprise, and Fanhua Xinlian Information Technology Consulting (Shenzhen) Co., Ltd., or Xinlian Information, cannot exceed statutory limits and must be registered with the State Administration of Foreign Exchange, or the SAFE, or its local counterparts. Under applicable PRC law, the Chinese regulators must approve the amount of a foreign-invested enterprise’s registered capital, which represents shareholders’ equity investments over a defined period of time, and the foreign-invested enterprise’s total investment, which represents the total of the company’s registered capital plus permitted loans. The registered capital/total investment ratio cannot be lower than the minimum statutory requirement and the excess of the total investment over the registered capital represents the maximum amount of borrowings that a foreign-invested enterprise is permitted to have under PRC law. Our directly-held PRC subsidiaries were allowed to incur a total of HK$300 million (US$38.4 million) in foreign debts as of March 31, 2018. If we were to provide loans to our directly-held PRC subsidiaries in excess of the above amount, we would have to apply to the relevant government authorities for an increase in their permitted total investment amounts. The various applications could be time-consuming and their outcomes would be uncertain. Concurrently with the loans, we might have to make capital contributions to these subsidiaries in order to maintain the statutory minimum registered capital/total investment ratio, and such capital contributions involve uncertainties of their own, as discussed below. Furthermore, even if we make loans to our directly-held PRC subsidiaries that do not exceed their current maximum amount of borrowings, we will have to register each loan with the SAFE or its local counterpart within 15 days after the signing of the relevant loan agreement. Subject to the conditions stipulated by the SAFE, the SAFE or its local counterpart will issue a registration certificate of foreign debts to us within 20 days after reviewing and accepting our application. In practice, it may take longer to complete such SAFE registration process.

| -14- |

Any loans we make to any of our indirectly-held PRC subsidiaries (those PRC subsidiaries which we hold indirectly through Zhonglian Enterprise and Xinlian Information), all of which are treated as PRC domestic companies rather than foreign-invested enterprises under PRC law, are also subject to various PRC regulations and approvals. Under applicable PRC regulations, medium- and long-term international commercial loans to PRC domestic companies are subject to approval by the National Development and Reform Commission. Short-term international commercial loans to PRC domestic companies are subject to the balance control system effected by the SAFE. Due to the above restrictions, we are not likely to make loans to any of our indirectly-held PRC subsidiaries.

Any capital contributions we make to our PRC subsidiaries, including directly-held and indirectly-held PRC subsidiaries, must be approved by the PRC Ministry of Commerce or its local counterparts, and registered with the SAFE or its local counterparts. Such applications and registrations could be time consuming and their outcomes would be uncertain.

We cannot assure you that we will be able to complete the necessary government registrations or obtain the necessary government approvals on a timely basis, if at all, with respect to future loans by us to our PRC subsidiaries, or with respect to future capital contributions by us to our PRC subsidiaries. If we fail to complete such registrations or obtain such approvals, our ability to capitalize or otherwise fund our PRC operations may be negatively affected, which could adversely and materially affect our liquidity and our ability to fund and expand our business.

On August 29, 2008, SAFE promulgated Circular 142, a notice regulating the conversion by a foreign-invested company of its capital contribution in foreign currency into RMB. The notice requires that the capital of a foreign-invested company settled in RMB converted from foreign currencies shall be used only for purposes within the business scope as approved by the authorities in charge of foreign investment or by other government authorities and as registered with the State Administration for Industry and Commerce and, unless set forth in the business scope or in other regulations, may not be used for equity investments within the PRC. In addition, SAFE strengthened its oversight of the flow and use of the capital of a foreign-invested company settled in RMB converted from foreign currencies. The use of such RMB capital may not be changed without SAFE’s approval, and may not in any case be used to repay RMB loans if the proceeds of such loans have not been used. Violations of Circular 142 will result in severe penalties, including heavy fines. As a result, Circular 142 may significantly limit our ability to provide additional funding to our PRC subsidiaries through our directly-held PRC subsidiaries in the PRC, which may adversely affect our ability to expand our business.

However, on March 30, 2015, SAFE promulgated Circular 19, a notice on reforming the administrative approach regarding the settlement of the foreign exchange capitals of foreign-invested enterprises, which became effective on June 1, 2015. The new notice states that foreign-invested enterprises shall be allowed to settle their foreign exchange capitals on a discretionary basis. The discretionary settlement by a foreign-invested enterprise of its foreign exchange capital shall mean that the foreign-invested enterprise may, according to its actual business needs, settle with a bank the portion of the foreign exchange capital in its capital account for which the relevant foreign exchange bureau has confirmed monetary contribution rights and interests (or for which the bank has registered the account-crediting of monetary contribution). For the time being, foreign-invested enterprises are allowed to settle 100% of their foreign exchange capitals on a discretionary basis. The SAFE may adjust the foregoing percentage as appropriate according to balance of payments situations. As a result, Circular 19 will relax the limitation of our ability to provide additional funding to our PRC subsidiaries through our directly-held PRC subsidiaries in the PRC.

| -15- |

Risks Related to Doing Business in China

Adverse economic, political and legal developments in China could have a material adverse effect on our business.

Substantially all of our business operations are conducted in China. Accordingly, our results of operations, financial condition and prospects are subject to a significant degree to economic, political and legal developments in China. China’s economy differs from the economies of most developed countries in many respects, including with respect to the amount of government involvement, level of development, growth rate, control of foreign exchange and allocation of resources. While the PRC economy has experienced significant growth in the past 30 years or so, growth has been uneven across different regions and among various economic sectors of China. Economic growth in China has been slowing in the past few years and dropped to 6.9% for 2017, according to data released by the PRC government in January 2018. The PRC government has implemented various measures to encourage economic development and guide the allocation of resources. However, these measures may not be successful in transforming the Chinese economy or spurring growth. While some of these measures benefit the overall PRC economy, they may also have a negative effect on us. For example, our financial condition and results of operations may be adversely affected by government control over capital investments or changes in tax regulations that are applicable to us.

Although the PRC government has implemented measures since the late 1970s emphasizing the utilization of market forces for economic reform, the reduction of state ownership of productive assets and the establishment of improved corporate governance in business enterprises, the PRC government still owns a substantial portion of productive assets in China. In addition, the PRC government continues to play a significant role in regulating industry development by imposing industrial policies. The PRC government also exercises significant control over China’s economic growth through the allocation of resources, controlling payment of foreign currency- denominated obligations, setting monetary policy and providing preferential treatment to particular industries or companies. Actions and policies of the PRC government could materially affect our ability to operate our business.